What Is an Investment Decision Control System?

By Team Acumentica

What Is an Investment Decision Control System?

The Next Evolution in Institutional Portfolio Management

Introduction

For decades, investment management has relied on an ecosystem of tools designed to analyze markets, evaluate risk, and assist portfolio managers in allocating capital. These tools; portfolio optimization software, risk analytics platforms, economic dashboards, and trading models—have become increasingly sophisticated. Yet despite these advancements, one structural limitation has persisted across the industry: most investment systems analyze markets but do not govern decisions.

In traditional asset management environments, decision-making remains fragmented. Risk systems calculate exposures. Optimization engines propose allocations. Analysts generate insights. Portfolio managers interpret the information and ultimately decide what action to take.

The process works, but it is inherently human-dependent, fragmented, and reactive.

As markets become more complex and data volumes expand exponentially, institutions are beginning to explore a new paradigm: Investment Decision Control Systems.

An Investment Decision Control System integrates analytics, optimization, and governance within a unified architecture designed to continuously evaluate market conditions, enforce constraints, and guide capital allocation decisions under uncertainty.

Rather than simply presenting information, these systems are designed to control how investment decisions are made.

This article explores:

• What an Investment Decision Control System is

• Why traditional portfolio tools are insufficient in modern markets

• How closed-loop financial architectures work

• The components required to build such systems

• Why this new approach may define the future of institutional investing

The Limitations of Traditional Portfolio Management Systems

Modern investment organizations operate with a wide range of specialized tools:

Risk management platforms

Portfolio optimization engines

Market data terminals

Economic research dashboards

Quantitative trading models

Portfolio management systems

Each of these tools performs a valuable function. However, they typically operate as independent analytical modules rather than coordinated decision systems.

This creates several structural challenges.

Fragmented Decision Processes

Most institutions operate within a multi-system analytical stack.

For example:

A risk platform evaluates portfolio exposures

An optimizer calculates potential allocations

A research team evaluates macro conditions

A portfolio manager interprets the information

While each component is valuable, the final decision process remains manual and subjective.

Even in highly quantitative firms, investment decisions often involve multiple tools and discretionary judgment layers.

Reactive Rather Than Adaptive Systems

Traditional systems also operate after conditions change.

For example:

Risk analytics report exposures once portfolios are constructed

Backtests analyze past performance

Stress tests simulate potential market shocks

These functions are valuable, but they are fundamentally diagnostic rather than controlling.

They describe outcomes rather than govern decisions before capital is deployed.

Increasing Complexity in Global Markets

Financial markets now operate in an environment characterized by:

rapid information diffusion

geopolitical uncertainty

algorithmic trading competition

macroeconomic volatility

nonlinear risk dynamics

These dynamics make manual decision coordination increasingly difficult.

As a result, institutional investors are exploring systems capable of continuously evaluating conditions and governing decision processes automatically.

This is where Investment Decision Control Systems begin to emerge.

Defining an Investment Decision Control System

An Investment Decision Control System is a financial architecture designed to continuously sense market conditions, evaluate portfolio constraints, generate allocation decisions, and adapt policies through feedback mechanisms.

Unlike traditional investment tools, which focus on analysis, a decision control system focuses on governance of actions.

In practical terms, such a system integrates multiple layers:

Market sensing systems

Predictive modeling engines

portfolio optimization modules

risk governance frameworks

adaptive learning mechanisms

These components operate together within a closed-loop architecture.

This structure is conceptually similar to control systems used in other complex industries.

Examples include:

aerospace flight control systems

autonomous vehicle navigation systems

industrial process control systems

robotics and adaptive manufacturing systems

In each of these domains, the system continuously:

senses the environment

evaluates system states

determines control actions

applies adjustments

learns from outcomes

Investment Decision Control Systems apply the same principle to capital allocation and portfolio governance.

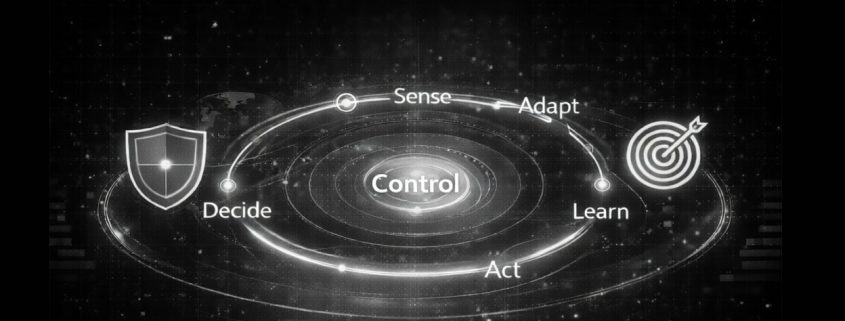

The Concept of Closed-Loop Investment Systems

A central principle of modern decision control systems is closed-loop feedback.

In traditional financial systems, analysis and execution are separated.

A closed-loop system integrates these components into a continuous decision cycle.

The cycle typically consists of five stages.

1. Market Sensing

The system continuously monitors inputs such as:

market prices

macroeconomic indicators

volatility regimes

news sentiment

liquidity conditions

factor exposures

These inputs form the state of the market environment.

2. Predictive Evaluation

Predictive models evaluate potential market developments.

These models may include:

statistical learning models

regime detection models

machine learning predictors

economic forecasting models

Their purpose is not to produce trading signals alone but to inform the decision framework.

3. Portfolio Optimization

Optimization engines evaluate how capital should be allocated given:

expected returns

risk constraints

transaction costs

diversification requirements

institutional investment mandates

This stage generates candidate allocations consistent with the system’s objectives.

4. Governance and Constraint Enforcement

Unlike simple optimizers, a decision control system enforces policy constraints.

These constraints may include:

volatility limits

drawdown restrictions

factor exposure boundaries

sector concentration limits

liquidity requirements

This ensures that allocations remain consistent with institutional governance policies.

5. Adaptive Learning

Finally, the system evaluates outcomes and adjusts decision policies over time.

This adaptive component allows the system to improve as market regimes evolve.

Architecture of an Investment Decision Control System

A complete system typically includes multiple integrated modules.

Market Intelligence Layer

This layer gathers and processes information from financial markets and macroeconomic environments.

Inputs may include:

equity and fixed income market data

economic indicators

geopolitical events

corporate fundamentals

sentiment analysis

The objective is to build a comprehensive representation of market conditions.

Predictive Modeling Layer

Predictive models help anticipate market dynamics.

Examples include:

time series forecasting models

regime detection models

volatility forecasting systems

machine learning price predictors

These models inform the decision process but are not the sole drivers of action.

Portfolio Optimization Layer

Optimization algorithms evaluate capital allocation strategies.

Examples include:

mean-variance optimization

risk parity models

hierarchical risk parity

multi-objective optimization frameworks

These models balance expected returns with risk constraints.

Governance Layer

This layer ensures that portfolio decisions remain consistent with institutional mandates.

For example:

capital allocation limits

exposure restrictions

drawdown protection rules

diversification constraints

The governance layer acts as the policy enforcement system for investment decisions.

Adaptive Control Layer

Finally, adaptive mechanisms allow the system to evolve.

This layer may incorporate:

reinforcement learning

Bayesian updating

performance attribution analysis

regime adaptation models

These capabilities help the system adjust its behavior as conditions change.

Why Investment Decision Control Systems Matter

The emergence of decision control architectures reflects broader changes in financial markets.

Increasing Data Complexity

Financial institutions must process:

massive market data streams

global macroeconomic signals

real-time trading information

alternative datasets

Manual interpretation of these inputs becomes increasingly difficult.

Control systems help manage this complexity.

Institutional Risk Governance

Institutional investors must adhere to strict governance frameworks.

These may include:

risk budgets

regulatory requirements

fiduciary constraints

diversification mandates

Decision control systems help enforce these policies consistently.

Adaptation to Market Regimes

Markets operate in different regimes:

growth environments

inflationary periods

liquidity crises

geopolitical shocks

Adaptive decision systems help portfolios adjust more effectively to these shifts.

Investment Decision Control vs Traditional Portfolio Systems

The difference between traditional systems and control architectures can be summarized simply.

| Traditional Systems | Decision Control Systems |

|---|---|

| Analyze markets | Govern decisions |

| Disconnected tools | Integrated architecture |

| Human interpretation required | Automated policy enforcement |

| Reactive analysis | Continuous adaptation |

This shift represents a structural evolution in investment technology.

The Future of Institutional Investment Systems

Many of the largest financial institutions are exploring architectures that integrate:

machine learning

portfolio optimization

risk governance

decision automation

While terminology varies across firms, the underlying concept increasingly resembles decision control systems.

As financial markets continue to evolve, the ability to govern capital allocation dynamically and systematically may become a defining capability of next-generation investment platforms.

Conclusion

Investment management has historically relied on tools that analyze information but leave decision coordination to humans.

As markets grow more complex and institutional portfolios face increasing governance requirements, a new paradigm is emerging.

Investment Decision Control Systems integrate sensing, prediction, optimization, governance, and adaptive learning within a unified architecture designed to guide capital allocation under uncertainty.

By transforming fragmented analytical workflows into structured decision processes, these systems represent a significant step toward more resilient, adaptive investment management frameworks.

The institutions that successfully implement such architectures may gain a structural advantage in navigating increasingly volatile global markets.

Learn More

If you are interested in learning how modern AI-driven Investment Decision Control Systems can help institutional investors govern portfolio decisions under uncertainty, you can learn more or contact us directly.

Visit:

to explore our research, technology, and institutional investment solutions.